The demographic alarm bells are ringing

The younger generations don’t see wine as the obvious choice to drink for dinners or parties, as mentioned before. The SVB considers this as a huge problem. Or rather, A HUGE PROBLEM.

“Unless the industry does more to attract consumers younger than 65, wine consumption might drop by 20 percent when boomers sunset.”

(The Boomer generation refers to people born between 1946 and 1964, in other words people who today are between 57 and 75. They are followed by X, millennials and Z.)

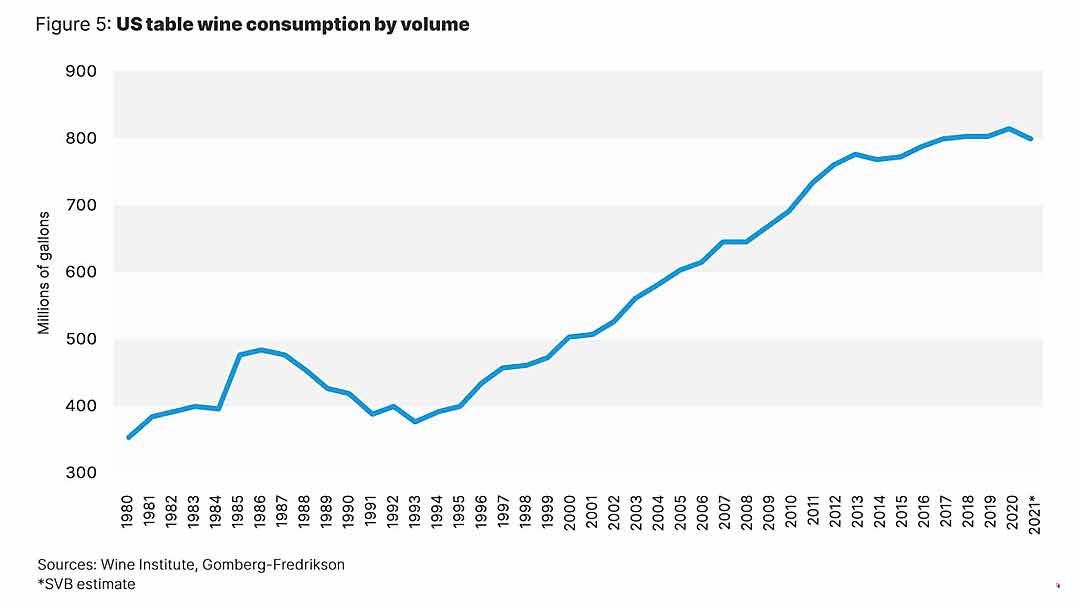

The USA is still the world’s biggest wine consumer, drinking 33 million hectolitres in 2020, according to the International Organisation of Vine and Wine (OIV), a year with zero growth. This follows a long period of good growth numbers. In 2000 the US consumed only just over 20 million hectolitres. In 2013, thanks to its rapid growth, the USA became the world’s biggest wine market, overtaking France.

Will the OIV figures for 2021, soon to be published, confirm the decline?

The bank points to one big issue: the wine industry is failing to attract the younger generations, failing in their marketing messages. The wine industry needs to come up with messages on issues like ethnic diversity, climate change and global warming, health and well-being, social justice, the environment and green issues and other themes that are important for the young people today, according to their analysis.

“The US wine industry isn’t doing a good enough job of marketing and selling its product, often remaining wedded to successful strategies from the past while the culture, country, business environment and consumer have radically evolved. It’s flat-out not good enough, and the overall industry results show it.”

“If we really want to reach the millennial, we need to move away from lifestyles of the rich and famous and add cause-based marketing to our outreach. We need to hire more people in tasting rooms with tattoos and with different ethnicities. We need to promote our efforts at being carbon- neutral and our support for social justice.” (The SVB US Wine Industry Report 2022)

A crisis not only for the US wine industry?

The declining US consumption is a critical message for the US wine industry but the consequences are so far-reaching that it should be a concern for the global wine industry.

As noted above, the US is the world’s biggest wine market, the biggest wine consumer. If consumption is flattening out or even decreasing in the long run wine producers all over the world will have to think hard about which markets to focus on.

This comes at a time when another of the world’s biggest wine markets have become a cause for concern: China. The Chinese market has for many years been seen as one of the big opportunities to grow wine sales. It has even become the biggest export market for Bordeaux wine. But that picture is changing. In 2020 the Chinese wine consumption slumped -17.4%, the third year in a row of declining consumption.

So if both the USA and China, two of the world’s biggest markets, are losing interest in wine, where should producers look for opportunities?

Grape and wine over-supply

The US has seen two years of small harvests. But, despite that, grape and bulk wine prices have not gone up. The conclusion seems to be that stock levels are still satisfactory (or more), and the producers are not predicting an increase in demand (consumption).

Looking back, the harvest volumes have seen at least four decades of steady growth, from 1.5 million tons in 1977 to 4.3 million tons in 2018. The grape crush is now down 20% from that peak.

The SVB quotes Jeff Bitter, president of Allied Grape Growers, arguing for reducing the acreage planted with wine. Grub up vineyards. This seems to be a clear indication that there is currently an over-supply of grapes. However painful the recent wildfires on the West Coast were, they must somewhat have alleviated the over-supply.

Or perhaps consumers can look forward to a period of lower wine prices if the abundance of grapes (and bulk wine) continues?

2 Responses

This was a fantastic summary write-up. Found it posted over in facebook. I’m headed over to read about WineRAMP. I thought the slumping sales in inexpensive wines as an indicator of problems for the industry later on because the industry failed to induct new drinkers was intriguing.

At some point our market will mature. It’s just a question of time.

Thank you. It’s interesting to see how sometimes data is a good illustration/confirmation of trends.